Table of Contents

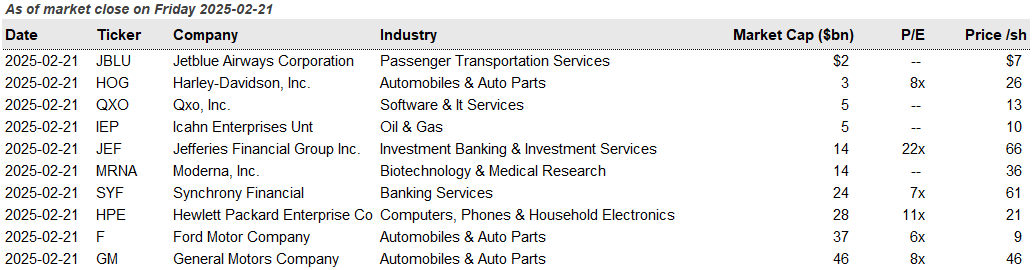

Y250221 / Teladoc Health was lost this week / Remaining companies include JetBlue, Harley-Davidson, Icahn Ent., QXO, Moderna, Jefferies, Synchrony Financial, HP Enterprise Co., Ford, and General Motors

Below is the weekly output for Screener C – where we keep a passive watch for companies trading (potentially) close to cash value.

This is one method we use to narrow our focus on companies for further investigation.

Screener C has the following criteria:

- Company has significant operations in the U.S. or is registered on a U.S. exchange

- Over $2.0bn market capitalization

- Share price to book value is less than 2.0x (current market price is below 2.0x book value)

- Share price to cash and equivalents per share less than 2.0x (current market price is below 2.0x cash per share)

Results for February 21, 2025

No new companies added to Screener C this week, however Teladoc Health Inc was lost. There are 10 companies, when compared to last weeks results, that still meet Screener C criteria above.

- Screener results: 10 companies

- New this week: 0 companies

- Lost this week: 1 company (TDOC)

Select individual company name for amplifying information

1 Harley-Davidson Inc. (HOG) – remains on list

First appearing on the list in October 2023 (Y231029) and intermittently thereafter, Harley-Davidson manufacturers motorcycles, motorcycle parts, accessories and apparel. Based in Milwaukee, WI, the company is one of the leading motorcycle manufacturers in the world and is well-recognized for it’s iconic brand. The parent company consists of a manufacturing company (HDMC), a financing business (HDFS) and a majority stake in LiveWire a U.S. electric motorcycle company. Sales have essentially been stable over the past 10 years, excluding 2020 when supply chain shocks and consumer demand hit particularly hard. The common stock pays a dividend and the company has been repurchasing some shares over the past two years. Management has been very focused on cost cutting and maintaining profitability, while higher interest rates have materially pressured recreation industry participants.

COMMENT: The financing business certainly needs more diligence. At initial glance however, a healthy cash position and debt / EBITDA levels below 1.5x for the manufacturing and sales side of the house, appear to be a comfortably low level.

2 QXO Inc. (QXO) – remains on list

QXO (formerly Silversun Technologies, Inc. – SSNT) is a value-added reseller (VAR) of business software, offering solutions for accounting, business management, financial reporting, managed services, and other services to small and medium businesses. This business has recently transformed through an inventive transaction led by Brad Jacobs, the founder of United Waste Systems (now Waste Management), United Rentals, and other companies. The transaction was completed in June 2024, with Jacobs becoming CEO and board chairman, effectively transforming Silversun (with a previous market cap below $20mm) into a reorganized QXO with a large cash infusion. The company’s strategy is now to become tech-forward leader in the building products distribution industry via accretive acquisitions and organic growth.

3 Moderna Inc (MRNA) – remains on list

Intermittently on and off the list throughout 2023 and 2024. Moderna is a biotechnology company that researches and develops drugs. Headquartered in Cambridge, MA the company’s drugs are based on Messenger RNA (mRNA) – a key component studied within the field of molecular biology and used to deliver vaccine solutions for the COVID-19 pandemic. The company’s revenue is purely from their COVID-19 vaccine although they have recently gained FDA approval for a vaccine intended to treat RSV (respiratory syncytial virus). The company went public in December 2018 and has only achieved profitability on a GAAP basis for FY 2021 and 2022. Revenues have collapsed sharply since their 2022 high. Some believe mRNA can be used to create new medicine classes and drugs with the potential to materially improve human lives and open entirely new markets.

COMMENT: Because biotechnology company valuations can vary widely, often spiking and plunging on news related to regulatory approval or perceived drug performance results, we remain very hesitant on the sector broadly.

4 Hewlett Packard Enterprise Co (HPE) – remains on list

Appearing for the first time on this screen in December 2024, Hewlett Packard Enterprise Co provides computer hardware, software, and services for businesses and cloud / hybrid-cloud deployments. The San Jose, California company was originally spun out of Hewlett-Packard in 2015 and has recently gained attention for it’s AI-related infrastructure that is more tailored to enterprise clients than other computer hardware competitors. Revenues and earnings have been relatively flat for the past 7 years. HP pays a consistent dividend (~2.3%), has not repurchased stock, and has a comparatively low PE multiple (~12.0x LTM P/E) for the computer hardware / IT sector. The company is in the process of acquiring Juniper Networks – intended to compliment and scale the company’s existing networking business.

5 Teladoc Health Inc. (TDOC) – lost this week

Teladoc Health common stock sold off sharply this week and was down a further ~15%. With this recent price move, the total market capitalization has moved below $2.0bn and therefore no longer meets the criteria for this screen. Shares are now trading hands around $11.50 per share.

First appearing on the list in April 2024 (Y240420) and intermittently thereafter, Teladoc is a telehealth company using phone and video chat technology to provide on-demand remote medical care. Founded in 2002 and publicly listed via IPO in 2015, the NY headquartered company is the first and largest telehealth platform in the U.S., delivering on-demand health care anytime via the Internet. It provides consumers with access to its network of more than 2,650 board-certified, state-licensed physicians and behavioral health professionals who provide care for a wide range of non-emergency conditions. Revenues have increased on average ~25% over the past 5 years but the growth has been mostly inorganic and profitability on a GAAP basis has been nonexistent. There is no dividend and the company is a net issuer of common stock (no buybacks). Several acquisitions in the past few years have significantly added asset value, only to be subsequently written down.

Interpreting results

Broadly this is an output of U.S. companies with a current market equity value above $2.0bn, a moderately low market price relative to GAAP book value, and moderately low share price relative to cash per share. When compared to our YTB screens, screener C will identify smaller companies often related to financial services or related industries because of our price to cash threshold.

The output generally produces potential targets that require a particularly high level of analysis. Operating models and capital structures of anything on screener C need particular scrutiny. Every so often, we find an interesting company that is facing temporary challenges and / or circumstantial headwinds. These instances warrant timely and careful investigation.

Why this screen can be helpful

We find watching this output over time, allows us to quickly identify potential companies or situations to investigate further, augments the weekly Value Line publication well, and keeps us informed on the less-loved corners of the public markets without having to watch misleading charts or spin our wheels on short-term market movements. We like to observe new entrants and subsequent exits to the list, over time, and share with our trusted readers.