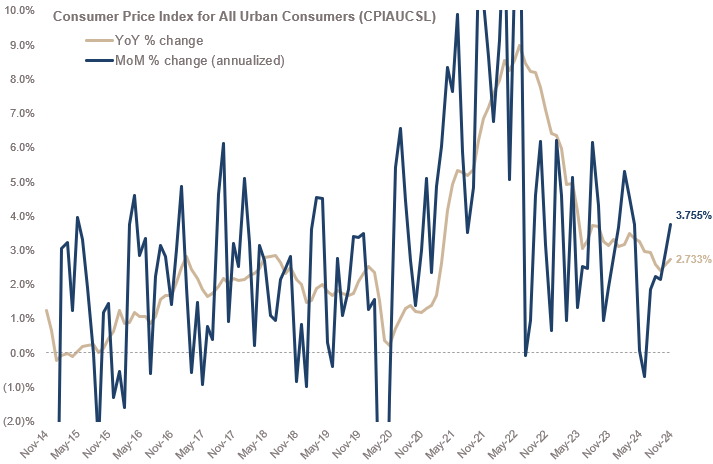

Y241213 / CPI for all urban consumers registered 0.313% for November 2024 / 3.755% annualized MoM increase / an acceleration from October’s reading /

Below is the Consumer Price Index (CPI) for all urban consumers for the last 10 year period, ending with the most recent data in November 2024.

This data is subject to revision by the U.S. Bureau of Economic Analysis (BEA) and was last accessed December 13, 2024.

Scroll past the chart for amplifying information on data source and interpreting the output.

Consumer Price Index for All Urban Consumers (CPI) – November 2024

Percent change MoM annualized (blue) and percent change YoY (gold)

Data Source

The Consumer Price Index is produced by the Bureau of Economic Analysis (BEA), which revises previously published data to reflect updated information or new methodology.

Available here

The data shown above is seasonally adjusted, reported on a monthly frequency, and indexed to 1982-1984 price levels.

Interpreting results

The Consumer Price Index for All Urban Consumers (all items) represents the price level of a basket of goods and services paid by urban consumers. Percent changes in the price index measure the inflation rate between any two time periods. The most common inflation metric is the percent change from one year ago. It can also represent the buying habits of urban consumers. This particular index includes ~88% of the total U.S. population, accounting for wage earners, clerical workers, technical workers, self-employed, short-term workers, unemployed, retirees, and those not in the labor force.

Why this output can be helpful

The CPI can be used to recognize periods of inflation, disinflation, and deflation. Because the CPI includes volatile food and oil prices, it may not most accurately represent underlying inflation. For a more accurate representation, the U.S. Federal Reserve typically reference the Core PCE Price Index. The CPI is a statistical measure vulnerable to sampling error.

COMMENT: The future inflation or disinflation we may or may not experience, in our view, will likely have highly material impacts on the cost of debt for all borrowers (governments, corporations, consumers, etc.). We see inflation as the most important factor for the cost of borrowing, excluding issuer specific risks, and believe expected future returns on all investment will be negatively impacted should inflation stay elevated or materially rise.